The Ultimate Guide to Retirement Planning: Strategies for a Secure Future

Retirement planning is a crucial aspect of financial management that ensures you can maintain your lifestyle after you stop working. Whether you’re just starting out or nearing retirement, understanding the key steps and strategies involved in retirement planning can make all the difference. This guide will provide you with comprehensive insights into how to plan for a secure future.

Understanding Your Retirement Needs

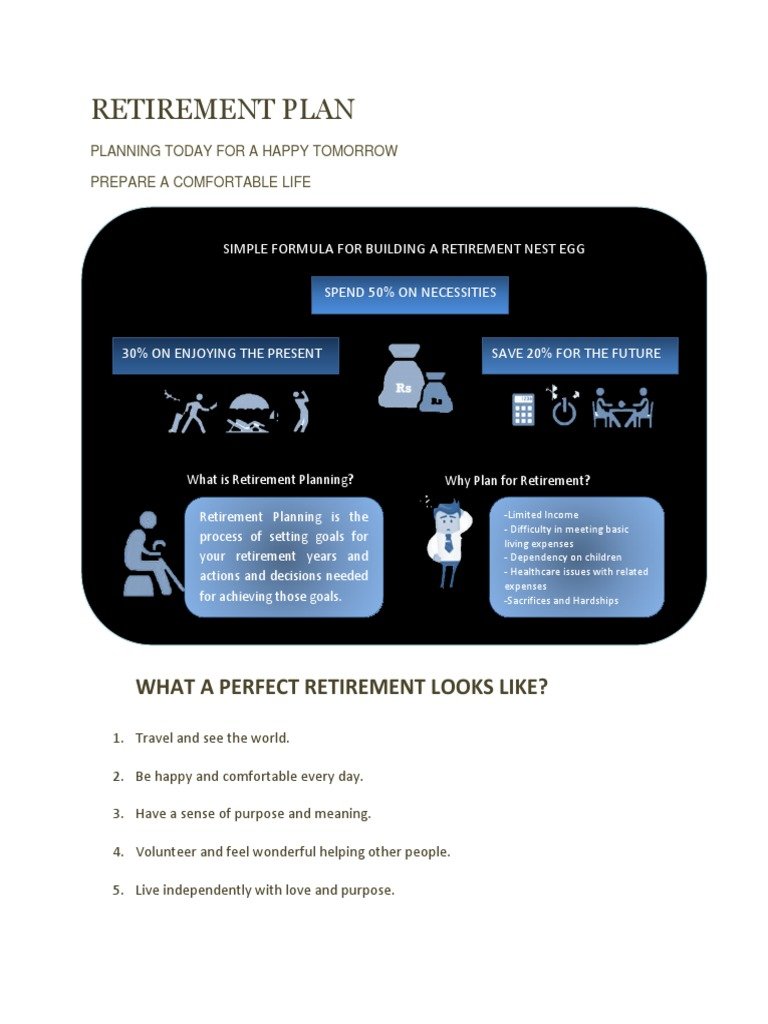

The first step in retirement planning is to estimate your financial needs. A common rule of thumb is that retirees need about 80% of their pre-retirement income to maintain their standard of living. To calculate this, start by estimating your total annual living expenses in retirement. Subtract any expected Social Security benefits and pension income from this amount to determine your net annual living expenses.

To get a more accurate picture, use your latest Social Security statement, which provides an estimate of your potential Social Security income. Once you have your net annual living expenses, multiply this figure by 25 to determine the total amount of money you need to save for retirement. This calculation is based on the 4% rule, which suggests that you should not withdraw more than 4% of your retirement savings per year to ensure it lasts for at least 30 years.

Saving and Investing for Retirement

Saving for retirement is different from investing. While saving involves setting aside money, investing requires putting that money into assets that can grow over time. Simply depositing money into a savings account may not be sufficient due to inflation and the potential for low returns. Instead, consider investing in the stock market, which has historically provided higher returns over the long term.

For example, if you contribute $5,000 per year to a savings account with a 1% interest rate, you would end up with approximately $208,000 after 35 years. However, if you invested the same amount annually with a 7% average return, you could have close to $700,000. It’s important to diversify your investments to manage risk and optimize growth. Consider a mix of stocks, bonds, and other assets to create a balanced portfolio.

Before you begin investing, it’s advisable to have three to six months of living expenses saved in a high-yield savings account. This provides a financial cushion against unexpected expenses without having to dip into your retirement funds.

How Much to Save Each Month

The amount you should save each month for retirement varies depending on your age, target retirement age, and current savings. As a general guideline, most Americans aim to save and invest 15% of their income for retirement. If this seems overwhelming, start with smaller contributions and gradually increase them over time.

If your employer offers a retirement plan with matching contributions, ensure you contribute enough to receive the full match. This is essentially free money that can significantly boost your savings. For those without employer-sponsored plans, aim to save at least 6% of your income, which is the average contribution rate in the U.S. Increase your contributions by 1 percentage point each year until you reach your desired rate, and consider boosting your contributions whenever you receive a raise.

Strategies for Late Starters

If you’re approaching retirement with less savings than desired, there are still effective strategies to catch up. Begin by assessing your current financial situation, including your net worth and retirement savings. Create a realistic budget that allows you to redirect funds towards retirement savings. Maximize contributions to retirement accounts like 401(k)s and IRAs, and take advantage of catch-up contributions if you’re 50 or older.

Diversify your investments to manage risk and consider part-time work or side gigs to generate additional income. Reducing debt, especially high-interest debt, can free up more money for savings. Leverage home equity through options like HELOCs or reverse mortgages, but consult a financial advisor to understand the implications. Stay informed about Social Security benefits and consider delaying them to increase monthly payouts. Finally, consulting a financial advisor can provide personalized guidance and help you create a tailored retirement strategy.

Retirement Planning for Small Business Owners

Small business owners and gig economy workers face unique challenges when it comes to retirement planning. Without company-sponsored plans, they must take the initiative to save independently. Several retirement account options are available, including SEP IRAs, Solo 401(k)s, SIMPLE IRAs, Roth IRAs, and Traditional 401(k)s. Each option has its own advantages and contribution limits, so it’s essential to choose the one that best fits your business model and financial goals.

Hiring a professional, such as a certified financial planner, can provide valuable insights and help navigate the complexities of retirement planning. Diversifying investments and choosing retirement plans tailored to small businesses can further enhance your savings strategy. Avoid relying solely on selling your business as a retirement plan, as this can be complicated and may not yield the expected results.

By understanding your financial needs, saving and investing wisely, and exploring the various retirement planning options available, you can build a secure and comfortable retirement. Start today and take the necessary steps to ensure a financially stable future.