The Ultimate Guide to Effective Tax Planning for Individuals and Businesses

Tax planning is a critical component of financial management that can significantly impact your bottom line. Whether you’re an individual or a business owner, strategic tax planning helps you minimize your tax liability while maximizing your savings. This guide will walk you through the essential steps to create a personalized tax plan that aligns with your financial goals.

Assess Your Current Financial Situation

Before diving into tax planning, it’s crucial to understand your current financial standing. Start by gathering all sources of income, including wages, investment returns, rental income, and freelance earnings. This step ensures you have a clear picture of your total income for the year.

Calculate Your Total Income from All Sources

- Wage Income: Include your regular salary and any additional income from side jobs.

- Investment Income: Consider dividends, capital gains, and interest from savings accounts.

- Rental Income: Document all income generated from property rentals.

- Freelance Work: Track payments received from contract work or consulting gigs.

For 2025, knowing your exact total income is essential for determining which deductions and credits apply to you. Understanding how different types of income affect your tax bracket can help you make informed decisions about your financial strategy.

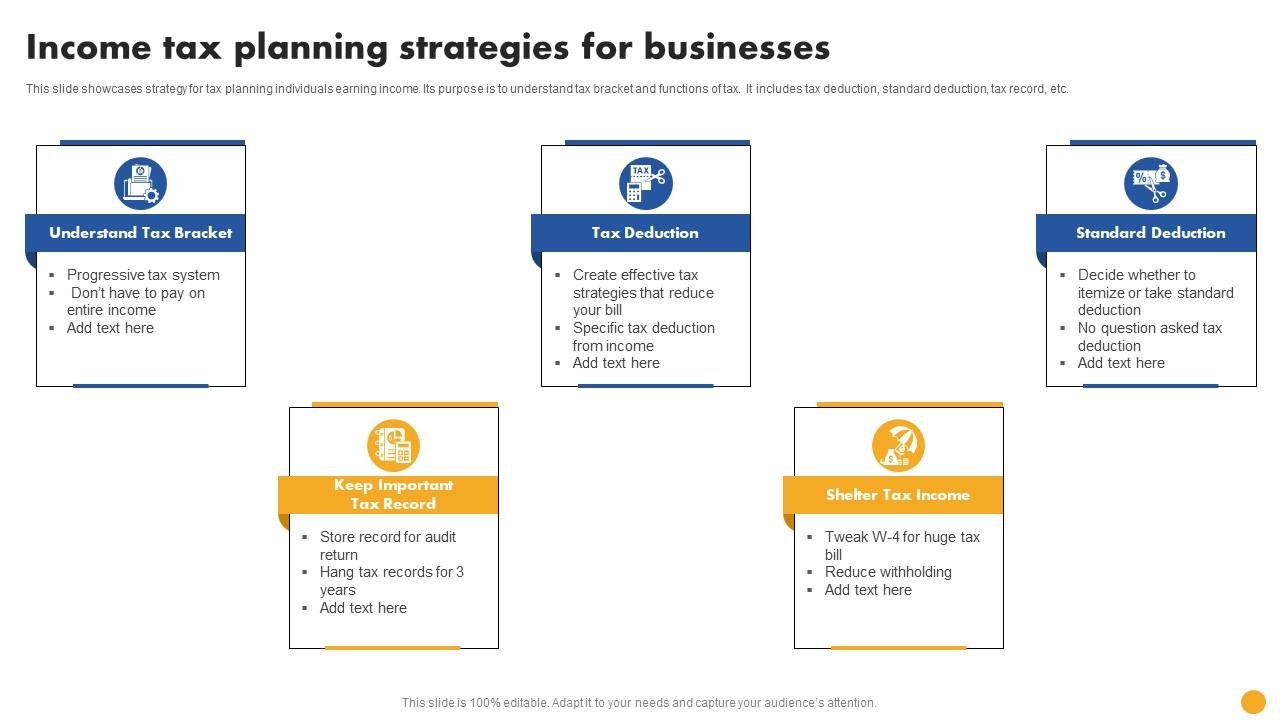

Identify Tax Deductions You Qualify For

Deductions reduce your taxable income, so identifying the ones you qualify for can save you significant money. Many people overlook opportunities to itemize deductions instead of taking the standard deduction.

Key Deductions to Consider

- Mortgage Interest: If you own a home, mortgage interest can be a substantial deduction.

- Property Taxes: These are deductible if you itemize.

- Charitable Contributions: Donations to qualified organizations can reduce your taxable income.

- Medical Expenses: Expenses exceeding 7.5% of your adjusted gross income (AGI) may qualify.

For self-employed individuals, business expenses such as home office costs, vehicle expenses, and professional fees can also be deducted. Keeping detailed records is essential, as the IRS requires documentation for these deductions.

Review Your Filing Status and Dependents

Your filing status determines your tax brackets, standard deduction amount, and eligibility for certain credits. Choosing the right status can lead to significant tax savings.

Filing Status Options

- Single: Ideal for those who are unmarried and do not have dependents.

- Married Filing Jointly: Often results in lower tax liability for married couples.

- Head of Household: Suitable for unmarried individuals who pay more than half the household expenses for a dependent.

If your marital status changed during the year, the status on December 31st determines your filing status for the entire year. Additionally, each dependent can reduce your taxable income through the standard deduction and may qualify for the child tax credit.

Build Your Tax Strategy Around Retirement and Investment Moves

Retirement planning is a vital aspect of tax strategy. Maximizing retirement contributions can significantly reduce your taxable income.

Maximize Retirement Contributions

- 401(k): For 2026, you can contribute up to $23,500, with an additional $7,500 catch-up contribution if you’re 50 or older.

- Traditional IRA: Offers a $7,500 annual contribution limit, with an extra $1,000 if you’re 50 or older.

Contributing to retirement accounts not only reduces your taxable income but also helps build long-term wealth. Automating contributions throughout the year ensures you meet your limits without last-minute scrambles.

Use Tax-Loss Harvesting to Offset Investment Gains

Tax-loss harvesting involves selling investments at a loss to offset gains elsewhere in your portfolio. This strategy can help reduce your overall tax liability.

How Tax-Loss Harvesting Works

- Selling Losing Positions: If you realize $8,000 in capital gains, selling a stock position down $5,000 reduces your net gains to $3,000.

- IRS Rules: The IRS allows you to deduct up to $3,000 of net losses against ordinary income each year, with excess losses carrying forward indefinitely.

The wash-sale rule prohibits buying a substantially identical security within 30 days before or after the sale. However, this rule does not apply to cryptocurrency, offering unique opportunities for tax benefits.

Plan Tax Changes Around Major Life Events

Major life events such as marriage, divorce, buying a home, starting a business, or inheriting assets can trigger significant tax changes. Proactive planning around these events can help you navigate the complexities of tax law.

Key Life Events and Tax Implications

- Marriage: Filing jointly often results in better tax outcomes, but consider both scenarios if one spouse has significant losses.

- Home Purchase: Mortgage interest becomes deductible, potentially shifting you from the standard deduction to itemizing.

- Inheritance: Inheriting an IRA after 2019 triggers the 10-year rule, requiring you to empty the account by the end of year 10.

Timing your decisions strategically can lead to substantial tax savings. Working with a tax professional can help you navigate these changes effectively.

State and Local Tax Planning Gets Overlooked

Many people focus exclusively on federal taxes and neglect state and local tax planning. Understanding your state’s tax rules can help you optimize your overall tax strategy.

State and Local Tax Considerations

- SALT Deduction Cap: For 2025, the SALT deduction cap remains at $10,000, regardless of actual state and local taxes paid.

- Income Allocation: If you’re self-employed and moved states during the year, your income allocation between states affects your total tax burden.

Proper state tax planning requires understanding your specific state’s rules before year-end. This knowledge can help you avoid unexpected tax liabilities and maximize your savings.

Home Office and Vehicle Deductions Create Major Savings

Business expenses and home office deductions represent significant opportunities for self-employed individuals and small business owners. The IRS offers simplified options and actual expense calculations to help you maximize your deductions.

Home Office Deductions

- Simplified Method: $5 per square foot up to 300 square feet, yielding a maximum $1,500 deduction.

- Actual Expenses: Deduct 10% of mortgage interest, property taxes, utilities, insurance, repairs, and depreciation.

Vehicle Expenses

- Standard Mileage Rate: $0.70 per mile for business driving in 2025.

- Documentation: Maintain a mileage log to ensure compliance with IRS requirements.

Organize Business Expenses for Maximum Deductions

Keeping your business expenses organized is essential for maximizing deductions. Separating personal and business expenses ensures clarity and compliance.

Key Business Expenses

- Supplies and Software: These are typically immediate deductions.

- Professional Development: Costs related to improving your skills can be deducted.

- Equipment Purchases: Items lasting more than one year usually require depreciation.

Maintaining a separate business bank account and credit card creates an automatic audit trail, helping you avoid potential issues with the IRS.

Final Thoughts

Effective tax planning requires treating your taxes as a year-round priority rather than an April scramble. By implementing the strategies outlined in this guide, you can reduce your tax liabilities, improve cash flow, and optimize your financial outcomes.

Start by pulling together your income documents and running a preliminary tax calculation in September. Adjust your W-4 if needed, max out retirement contributions before December 31st, and identify tax-loss harvesting opportunities in your portfolio.

If you own a business or work from home, organize your expenses now to ensure deductions are documented and defensible. These actions compound over time and create thousands in cumulative tax savings. Working with a tax professional transforms planning from overwhelming to manageable, and Clear View Business Solutions helps individuals and small business owners build personalized tax strategies that actually work.

Contact Clear View Business Solutions to create a personalized tax plan tailored to your specific situation. The difference between reactive and proactive planning shows up directly in your bank account.